Direct answer – What did the WSI warehouse survey find?

WSI’s 2026 manufacturer warehouse survey found a structural mismatch between current distribution networks and the operating environment manufacturers now face. The headline numbers are sharp: 306 U.S. manufacturing leaders surveyed, 88% expecting warehouse footprint changes within 18 months, 75% saying their networks evolved organically rather than by design, and 53% reporting a warehouse-related compliance, audit, or safety event in the last two years.

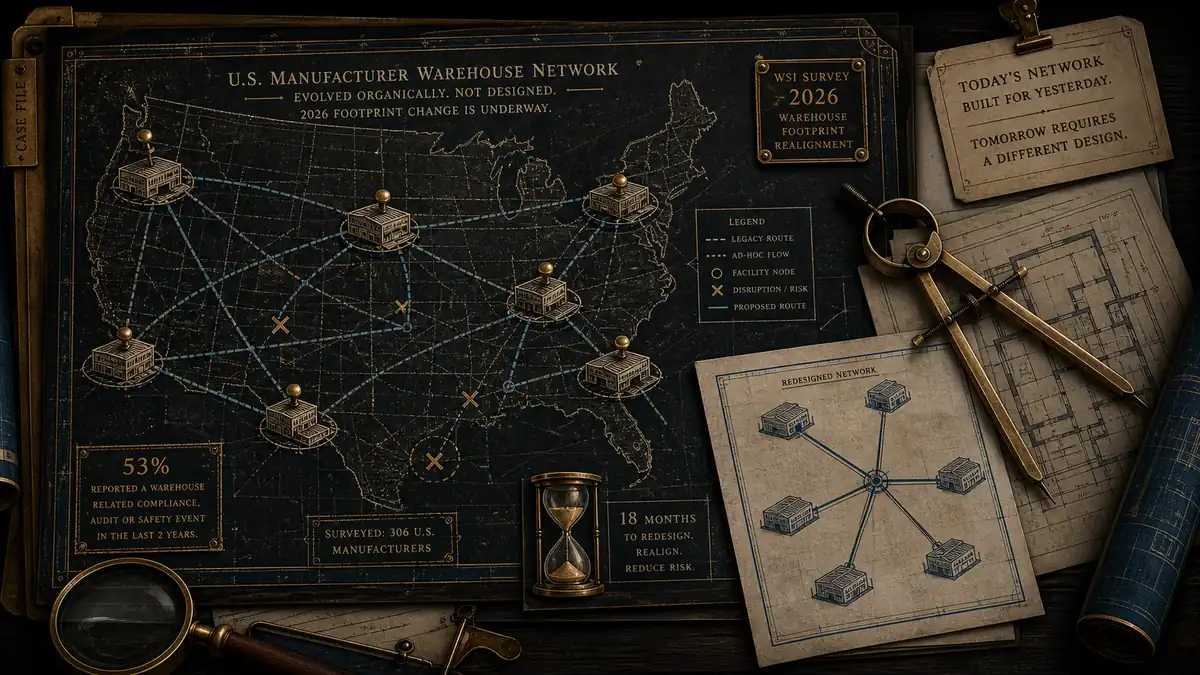

WSI released a 2026 warehouse network survey on June 17, 2026, based on responses from 306 supply chain, operations, and logistics leaders at U.S. manufacturing companies.

The survey covers manufacturers in chemicals, metals, food and beverage, building materials, electronics, and other industrial sectors. The signal is not that every warehouse is failing. It is that many networks were assembled over time, under older assumptions, and are now being asked to handle tariffs, reshoring pressure, compliance risk, and service volatility.

For manufacturers, this is a planning problem before it is a building problem. A new WMS, 3PL, or automation project can help, but only after the company understands where inventory should sit, which work should be outsourced, and which facilities are carrying hidden risk.

Key Takeaways

- WSI surveyed 306 U.S. manufacturing supply chain, operations, and logistics leaders.

- 88% expect their U.S. warehouse and distribution footprint to change within 18 months.

- 75% say their warehouse network evolved organically instead of being strategically designed.

- 67% have grown more likely to consider switching 3PL providers because of friction in the last 12 months.

- 53% reported a warehouse-related compliance incident, audit finding, or safety event in the last two years.

What WSI actually found

The survey’s strongest number is the 88% expecting a warehouse footprint change. That includes expansion, consolidation, or a shift in operating model. In other words, warehouse network redesign has moved from future-state planning into current work.

The second number explains why: 75% say their current network evolved organically. That is a polite way of saying that many manufacturers added buildings, lanes, 3PLs, and exceptions as the business grew, without ever resetting the network around today’s demand, compliance, and sourcing conditions.

The third number is the operational warning. More than half of respondents experienced a warehouse-related compliance incident, audit finding, or safety event in the last two years. That turns the warehouse from a cost center into a risk surface.

Why warehouse networks became a constraint

Organic networks are understandable. A plant adds a temporary storage site, a distributor asks for faster service in a new region, a customer requires special handling, a tariff change moves sourcing, and a 3PL gets added because the team needs capacity now. The network works until the exception load becomes the operating model.

That is why this survey should not be read as a simple “buy more warehouse automation” story. Automation can improve a well-designed flow, but it can also harden a bad layout. The same is true for WMS software: if the underlying inventory and process decisions are unclear, software mostly records the confusion faster. Big Joe’s 2026 autonomous material-handling launch makes the same point in equipment form: routes need to be understood before they are automated.

Factory Investigator has seen the same pattern in software buying. In our manufacturing software cost work, the integration line is where projects get expensive because ERP, warehouse, production, and quality workflows rarely line up as cleanly as the sales deck suggests.

The 3PL friction signal matters

The 67% 3PL-switching number may be the most commercially important finding. Switching a logistics provider is disruptive, so a high willingness to consider it usually means manufacturers are feeling pain in documentation, responsiveness, visibility, service consistency, or cost-to-serve.

But switching providers without redesigning the operating model can only move the friction. Manufacturers should separate three questions before issuing an RFP: what work should remain in-house, what work genuinely belongs with a 3PL, and what network shape supports the next 18 months of sourcing, demand, and compliance pressure.

That distinction matters for software too. If the real issue is material planning, MRP and ERP decisions may be upstream of the warehouse. If the issue is live production status, a shop-floor MES may need to feed warehouse planning more accurately. If the issue is customer promise dates, the answer may be all three systems plus cleaner operating rules. The Hitachi Norman AI-factory case shows that combined model in practice, joining inventory visibility, configuration automation and order-to-ship decisions.

What manufacturers should do now

Start with a network map, not a vendor list. Mark every warehouse, overflow site, 3PL location, cross-dock, supplier-delivered stock point, and customer-specific inventory rule. Then add three overlays: compliance exposure, service commitments, and cost-to-serve.

Next, classify each facility or partner by the job it is supposed to do. Some locations exist for speed, some for low-cost storage, some for hazardous or regulated handling, and some because the company never retired an old workaround. The last group is where redesign usually pays back fastest.

Finally, treat any 2026 warehouse project as a footprint decision first and a software or 3PL decision second. The goal is not to make a brittle network cheaper. The goal is to remove the brittleness before the next tariff, audit, customer requirement, or supply shock exposes it. Micron’s new-fab timing gap is the same lesson upstream: a larger footprint changes supply only after the process and supplier layers are qualified.

Frequently Asked Questions

It is a 2026 survey from WSI based on 306 U.S. manufacturing supply chain, operations, and logistics leaders. It examines warehouse footprint changes, 3PL relationships, compliance incidents, safety events, and how manufacturers are redesigning networks under cost, resilience, and reshoring pressure.

The biggest finding is that 88% of surveyed leaders expect their U.S. warehouse and distribution footprint to change within 18 months. That means redesign is no longer theoretical. Most manufacturers are already expecting expansion, consolidation, or operating-model changes.

If a warehouse network evolved organically, it may reflect old customers, old sourcing assumptions, temporary overflow decisions, and legacy 3PL relationships. That creates structural inefficiency. Optimization helps only after the manufacturer decides what the network is supposed to do now.

Not automatically. The survey shows high 3PL friction, but switching providers without redesigning the warehouse operating model can move the same problem to a new vendor. Manufacturers should map network roles, compliance exposure, and service requirements before running a 3PL search.