Direct answer – What does the June 2026 ISM manufacturing forecast say?

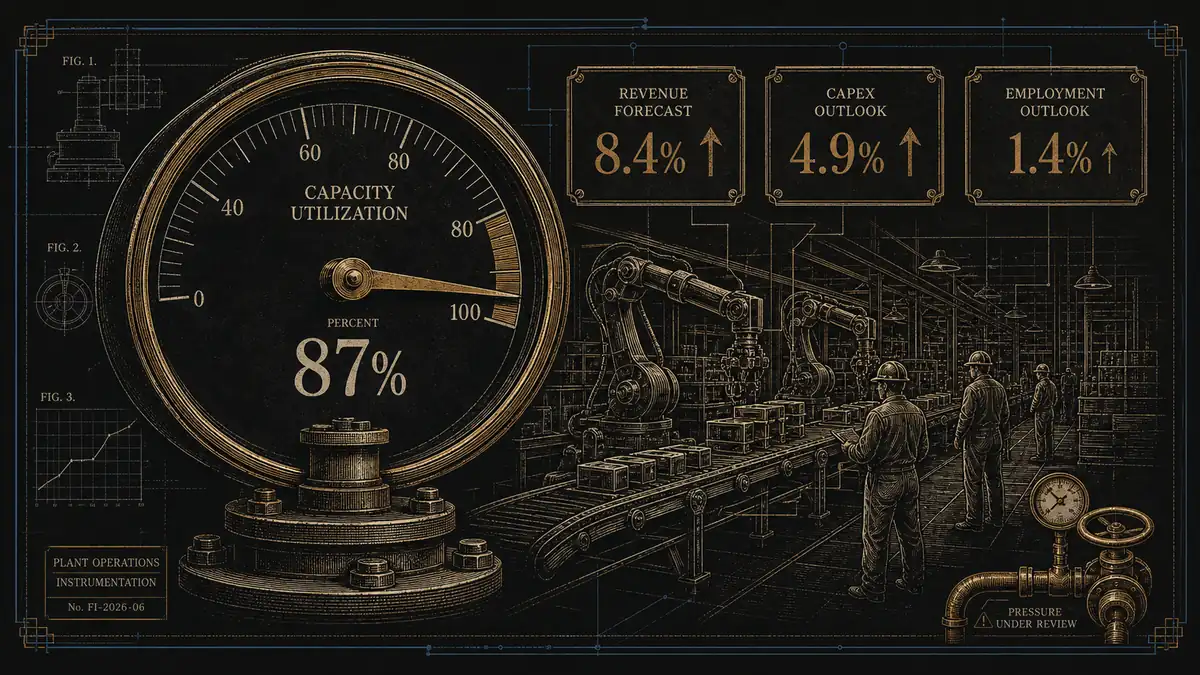

The June 2026 ISM Supply Chain Planning Forecast says U.S. manufacturing executives expect revenue to rise 8.4% in 2026, with plants operating at 86.9% of normal capacity and capital expenditures expected to increase 4.9%. The catch is labor and input pressure: manufacturing employment is forecast to rise only 1.4%, while raw-material prices are expected to increase 14.1% for the year.

The Institute for Supply Management released its Spring 2026 Supply Chain Planning Forecast on June 17, 2026, saying manufacturing is expected to expand over the rest of the year.

The headline numbers are positive: manufacturing revenue is expected to rise 8.4%, capital expenditures 4.9%, production capacity 9.7%, and operating rate is already at 86.9% of normal capacity. But the labor number is much smaller, with employment expected to increase only 1.4% by year-end.

For plant leaders, that mix points to a specific operating problem: more output and investment without much hiring cushion. It is a productivity, scheduling, automation, and margin-management story, not just an economic forecast.

Key Takeaways

- ISM projects 8.4% manufacturing revenue growth for 2026, up from the 4.4% forecast in December 2025.

- Manufacturers reported operating at 86.9% of normal capacity, 4.5 percentage points higher than December.

- Capital expenditures are expected to rise 4.9%, while production capacity is expected to rise 9.7%.

- Manufacturing employment is expected to increase only 1.4% in 2026.

- Raw-material prices are expected to rise 14.1% for the year, keeping margin pressure in the foreground.

What ISM actually reported

ISM’s forecast is built from purchasing and supply executives who also feed the monthly ISM PMI reports. The June update is stronger than the December 2025 forecast: expected manufacturing revenue growth doubled from 4.4% to 8.4%.

The operating-rate number is just as important. Manufacturers are operating at 86.9% of normal capacity, up from 82.4% in December. The six industries above that average include nonmetallic mineral products, paper products, primary metals, transportation equipment, computer and electronic products, and fabricated metal products.

ISM also says 14 of 18 manufacturing industries expect revenue increases for the rest of 2026. That makes the report a broad expansion signal, not a one-sector bounce.

The hidden signal: capacity is rising faster than hiring

The labor number changes how manufacturers should read the forecast. Revenue is expected to increase 8.4%, production capacity 9.7%, and capital expenditures 4.9%, but employment only 1.4%. If those numbers hold, the extra output has to come from better utilization, better planning, automation, overtime discipline, or process improvement.

ISM’s AI questions add another clue. The report says 51% of manufacturing respondents use generative AI chatbots, 45% use AI agents, and 76% say AI has not yet had a noticeable effect on hiring or layoff decisions. That suggests AI is present, but not yet a simple replacement for labor planning.

Our read: the forecast rewards manufacturers that can turn capex into throughput without losing control of inventory, quality, or lead times. The shops still reconciling production in spreadsheets will feel the pressure first. Hitachi’s 77% lead-time result is the kind of outcome that attracts attention, but its baseline and transfer conditions still need to be tested before another plant budgets against it.

What it means for plant investment

A 4.9% capex increase does not mean every manufacturer should rush into a major software or automation purchase. It means every investment should be tied to a constraint: planning accuracy, machine uptime, labor availability, warehouse friction, quality escapes, or quote-to-cash speed.

The software layer matters because capacity pressure exposes disconnected systems. A manufacturer choosing ERP for a small or scaling plant should ask whether the system improves scheduling, purchasing, inventory visibility, and cost control before adding modules. A shop comparing MES options should ask whether real-time production data will reduce downtime or just create another dashboard.

Cost discipline still matters. In our manufacturing software pricing work, implementation and integration were often the lines that turned a reasonable license into a heavy first-year bill. In a high-capacity environment, that bill is only defensible if the project removes a measured bottleneck.

What manufacturers should watch next

The first number to watch is raw-material inflation. ISM says prices paid increased 11.9% through June and are expected to rise 14.1% for all of 2026. Revenue growth looks better when input costs are stable; it looks thinner when material cost outruns the ability to reprice customers.

The second number is employment. If hiring stays flat while demand stays strong, overtime, quality, maintenance, and scheduler workload become the stress points. Manufacturers should track not just orders and revenue, but late jobs, expedites, premium freight, scrap, and rework.

The third number is system readiness. If AI agents, ERP upgrades, MES, or automation are part of the capex plan, define the operating metric before the purchase. “More AI” is not a plant strategy. Fewer late jobs, faster changeovers, lower scrap, better material availability, and cleaner capacity planning are.

Frequently Asked Questions

It is ISM’s forecast based on responses from purchasing and supply executives in manufacturing and services. The report tracks expected revenue, capital expenditures, capacity, employment, prices, and related operating conditions for the rest of the year.

ISM says manufacturing revenue is expected to increase 8.4% in 2026. That is 4 percentage points higher than the December 2025 forecast of 4.4%, and the report says 14 of 18 manufacturing industries expect revenue growth for the rest of the year.

It means manufacturers are already operating at a high share of normal capacity. When that combines with expected revenue growth and only modest hiring, plants need better scheduling, uptime, inventory accuracy, and throughput discipline to absorb demand without hurting quality or margins.

Not automatically. The forecast supports investment, but only where a clear constraint exists. Manufacturers should connect any ERP, MES, AI, or automation spend to a measurable target such as fewer late jobs, lower scrap, faster changeovers, better material availability, or reduced premium freight.